| |

Depreciation AccountingMeaningDepreciation in accounting refers to a continuous loss in the value of fixed assets to a certain period. It is an accounting method used to allocate the cost of assets over its useful life. It represents the value of an asset that has been used. The companies depreciate their long-term assets for tax as well as accounting purposes. The value of the depreciation is a fixed cost for the organizations and the amount depreciated can be used to buy a new machine once the old became obsolete. Generally, the assets lose their value due to normal wear and tear, continuous use, etc.

A point should be noted her is that the depreciation is a non-cash expense for the company but instead of this, it is considered as a business expense. Characteristics of Depreciation

Causes of Depreciation

Importance or Objectives of Depreciation1. Ascertaining the True Profit and Loss The true picture of profit and loss of the business can only be getting after debiting all the expenses incurred for earning revenues to the P & L Account. Depreciation is also an expense for the business that should be treated like all the other expenses so that the actual profit or loss can be calculated. 2. Showing the True and Fair Value of the Financial Position If the company does not charge the depreciation on the assets then the value transferred to the balance sheet will show an excess amount of their true values. Hence, the depreciation helps in ascertaining the true and fair value of the financial position of the company. 3. Accurate Cost of Production The correct cost of production can't be calculated unless depreciation is not charged. The sales price that the company will charge from the customers will be fixed at lower rates without taking depreciation into consideration which will cause a reduction in the profits. 4. Providing Funds for Replacement of Assets Depreciation is debited to the profit and loss account like other expenses but it is not charged in the form of cash. Hence, the amount of depreciation is retained in the business by transferring the depreciated amount to a new account named 'Provision for Depreciation Account'. The funds transferred to this account are used for the replacement of the assets after the expiry of their estimated life span. 5. Preventing the Distribution of Profits out of Capital If the proprietor does not charge depreciation on fixed assets, the surplus profit can be taken by the proprietor or paid to the shareholders as a dividend. As a result, the amount of dividend issued will include the portion of depreciation that should be transferred to the company's capital. As a result, depreciation must be calculated in order to avoid gains from being distributed profits out of capital. 6. Avoiding Over Payment of Income Tax Depreciation is a deductible expense for the tax purposes. If the company does not transfer the depreciation to the P&L Account then the value of net profit would be higher than the actual profit. Because of which higher income tax will be charged from the company. 7. Others If the depreciation is not calculated then the net profit in the P & L account will exceed the actual profits and as a result:

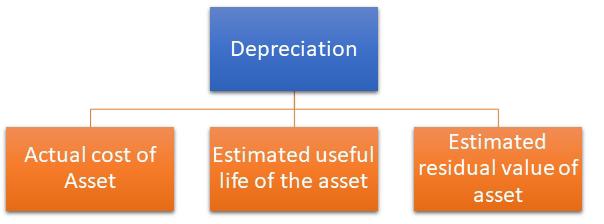

Factors Determining the Amount of Depreciation

1. Total Cost of the Asset The total cost of a fixed asset is calculated after including all the expenses that incurred for bringing the assets into the usable condition, such as transit insurance, freight, installation cost, etc. 2. Estimated Useful Life of Asset The useful life of the assets is calculated on the basis of number of years for which the assets can be effectively used for the production purposes. For example, if a machine can be used for 25 years but it become obsolete in 18 years due to an accident, change in technology, or any other reason then the useful life of that machine will be considered for only 18 years. 3. Estimated Scrap Value It is the estimated sale value of the assets after the expiry of its life span. This value is also called a residual value or break-up value. For example, if an asset is purchased for Rs. 50,000 and it has a serviceable life of 15 years. It is estimated that at the end of 15 years the scrap value of the asset will be Rs. 5,000. Depreciation in this case would be Rs. 3,000 per year. It can be calculated as follows: Depreciation = (50,000 - 5,000) / 15 = Rs. 3,000 per year Methods of Allocating Depreciation1. Straight Line Method Under this method, depreciation is charged at a fixed rate on the original cost of the asset for its whole life span. This method is also known as Original Cost Method, Equal Installment Method, and Fixed Installment Method. This method can be easily applied for those assets whose useful life can be estimated accurately. To calculate the value of depreciation through this method, the following formula is used: Deprecation = (Original Cost of Asset - Estimated Scrap Value) / Estimated Life Span of the Asset 2. Written Down Value Method Under this method, the value of asset diminishes every year and the value of depreciation also decreases every year. This method is also known Reducing Installment Method or Diminishing Balance Method. This method is suitable to use for the assets with long life span which demands less repair in further years, such as plant, land, building, etc. 3. Annuity Method Under this method of depreciation calculation, the rate of return of the asset is determined just like an investment. This method is generally used to determine the value of assets with large purchase value, long life, and a fixed rate of return. It demands the internal RoR on cash inflows and outflows of the asset. Then this IRR is multiplied with the initial book value of asset and the result is deducted from the cash flow of the period to calculate the value of the actual depreciation. 4. Depreciation Fund Method This method is also called sinking fund method. It is the technique of depreciating as asset while generating money to replace it at the end of its life span. As the depreciated amount shows the reducing value of an asset over the period, the same balance is invested. Such funds are invested in the sinking fund account so that the interest can be earned on it. 5. Insurance Policy Method Under this method, an insurance policy is taken for the period till when the asset gets matured to be replaced. Insurance policy method is similar to sinking fund method but here the amount of investment is in the form of premium paid on the insurance policy. The payment of this premium is made at the beginning of each year and debited to Depreciation Fund Policy Account. At the end of the accounting year, the annual depreciation of the asset and amount of annual premium are equal and is debited to P&L Account while credited from Depreciation Fund account. 6. Revaluation Method It is one of the easiest methods to calculate the depreciation. Under this method, the assets are revalued at the end of the financial year and then this balance is compared with the initial value of the assets at the beginning of the financial year. The difference between the values is considered as the amount of depreciation. It can be understood as: Revaluation = Opening Balance + Purchases - Closing Balance 7. Depletion Method This method is suitable for the wasting assets such as coal, mines, oil reserves, well, etc. Under this method, the rate of depreciation is determined by dividing the cost of an asset with the estimated quantity of the product that can be available. Then, the total output of that particular year is multiplied with the previously calculated rate of depreciation to get the actual amount of depreciation occurred. Generally, depletion is considered different from depreciation as it does not occur on tangible fixed assets. 8. Machine Hour Rate Method Under this method, the depreciation is calculated by determining the total life of any fixed asset on the basis of its working hour life or the number of hours for which the asset is being used. After this, the actual cost of fixed asset is divided by the life of fixed asset in hours to get the depreciation rate per hour of that asset. This method is suitable for machineries. The formula of machine hour rate method is as follows: Hourly Depreciation Rate = (Original Cost of Machine - Scrap Value) / Estimated Life of the Machine in Hours Methods of Recording Depreciation1. By Charging to Assets In this case, the company does not have to maintain 'Provision for Depreciation A/c'. Instead of it, depreciation is directly credited to 'Assets A/c' because of which the Asset A/c is presented at a written down value in the Ledger. 2. By Creating Provision for Depreciation Account In this method, the depreciation is credited to 'Provision for Depreciation A/c' and does not affect the balance of Asset A/c. Hence, Asset A/c shows an original cost in the Ledger. The balance appears on the credit side of the Provision for Depreciation A/c represents the total balance of depreciation accumulated to date. The total accumulated depreciation is transferred to the credit side of the Asset A/c if the asset is sold or discarded. The required entry in such case would be: Provision for Depreciation A/c or Accumulated Depreciation A/c Dr. To Asset A/c The remaining balance in the Provision for Depreciation A/c of that asset represents the accumulated depreciation of the unsold asset.

Next TopicInstitutional Shareholder Services

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share

Javatpoint Services

JavaTpoint offers too many high quality services. Mail us on [email protected], to get more information about given services.

- Website Designing

- Website Development

- Java Development

- PHP Development

- WordPress

- Graphic Designing

- Logo

- Digital Marketing

- On Page and Off Page SEO

- PPC

- Content Development

- Corporate Training

- Classroom and Online Training

- Data Entry

Training For College Campus

JavaTpoint offers college campus training on Core Java, Advance Java, .Net, Android, Hadoop, PHP, Web Technology and Python. Please mail your requirement at [email protected]

Duration: 1 week to 2 week