| |

What is ShareMeaning of ShareShare in the financial market refers to the small unit of ownership of a company. In other words, a share refers to the percentage of ownership in a company's financial assets. The investor who holds at least one share in a company is known as a shareholder. This investor can be a person, institution, or a company. Types of Shares1. Equity SharesEquity shares refer to those shares the amount of which is returned to the shareholders if the company's all assets get liquidated and its debt is paid off at the time of winding up of the company. These shares are mentioned under the Equity and Liability head of the Balance Sheet. Most of the equity shares provide voting rights to the shareholders. There is not any fixed rate of dividend provided by these shares and the company can also skip to pay the dividend if profit in a particular year is not sufficient. These shares are further divided into the following types:

2. Preference SharesPreference shares are those shares the dividend on which is paid before paying the dividend to the equity shareholders. In the case of bankruptcy or the winding up of the company, the payment is made to these shareholders from the company's assets prior to equity shareholders. Most of these shares have a fixed rate of dividend and the company is bound to pay it every year. However, preference shares do not offer any voting right to the shareholder. Preference shares are further divided into the following types:

Valuation of Shares

The process of knowing the real value of the company's shares refers to the valuation of shares. The value of shares can fluctuate with the market forces of demand and supply. It is easy to know the share price of a listed company but with private companies, it is an important and challenging task. This valuation is done by using various quantitative techniques which include the following three methods: 1. Asset-based MethodUnder this approach, share valuation is done by calculating the value of intangible assets and contingent liabilities. This approach is highly useful for manufacturers, distributors, etc. who use a large value of capital assets. The formula used under the asset-based method is as follows: Value per Share = (Net Asset - Preference Share Capital) / (Total Number of Equity Shares) 2. Income-based MethodWhen the valuation is done for a small number of shares, then this method can be useful. Here, the focus is on the income earned by the business from its investments, i.e., the profit generated by the business in the future. This approach can be further divided into two parts: Discounted Cash Flow (DCF) and Price Earning Capacity (PEC). The formula for the share valuation under the income-based approach is as follows: Value per Share = Capitalized Value / Total Number of Shares 3. Market-based MethodUnder this method, the share prices of the comparable public traded companies and the asset or stock sales of comparable private companies are used to calculate the value per share. The companies can easily collect the data of private companies from various proprietary databases but the main task is to choose comparable companies. Who is a Shareholder?Any person, company, or institution that holds or owns at least one share of a company's stock, is known as a shareholder in the company. Shareholders enjoy the benefits from the company's success in the form of increased stock valuation or dividends (profit distributed by the company to its shareholders). Conversely, when a company suffers a loss, the prices of the shares may drop invariably which can cause a decline in the value of the shares and also in the portfolios of the shareholders.

As per their stake in the company, the shareholders can be of two types: majority shareholders (those who hold majority shares in the company's stock, i.e., more than 50%) and minority shareholders (those who holds minority shares in the company's stock, i.e., less than 50%). Other than this, the shareholders can also be divided as per the types of shares they hold in the company. Those who hold the equity shares and have the voting right in the company's general meeting are known as common shareholders. While those who hold the preference shares and do not have the voting right are known as preferred shareholders. But, these shareholders have priority over the company's profit that is distributed in the form of dividends. Terminology

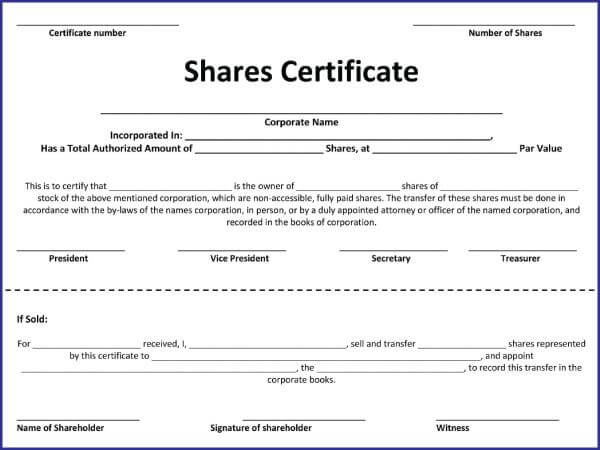

Tax Treatment of DividendsTax treatment of dividends varies between tax jurisdictions. In India, there is no tax charged on dividends in hands of shareholders up to INR 1 million. But the company which is using dividends has to pay dividends distribution tax at the rate of 12.5 percent. In our country, there is also the concept of a deemed dividend that is not tax-free. Further, the tax laws of the country include provisions to stop dividend stripping. What is Share Certificate?

Prior to the introduction of the Demat account and digital shares, a share certificate was issued to the investors as proof of their ownership in the company's shares. Now the concept of share certificates has been replaced with digital certificates. The ownership of the shareholders is recorded in electronic form by a system such as CREST or DTCC, a central securities depository. Difference between Shares and Stocks

Next TopicAccounting Principles

|

For Videos Join Our Youtube Channel: Join Now

For Videos Join Our Youtube Channel: Join Now

Feedback

- Send your Feedback to [email protected]

Help Others, Please Share

Javatpoint Services

JavaTpoint offers too many high quality services. Mail us on [email protected], to get more information about given services.

- Website Designing

- Website Development

- Java Development

- PHP Development

- WordPress

- Graphic Designing

- Logo

- Digital Marketing

- On Page and Off Page SEO

- PPC

- Content Development

- Corporate Training

- Classroom and Online Training

- Data Entry

Training For College Campus

JavaTpoint offers college campus training on Core Java, Advance Java, .Net, Android, Hadoop, PHP, Web Technology and Python. Please mail your requirement at [email protected]

Duration: 1 week to 2 week